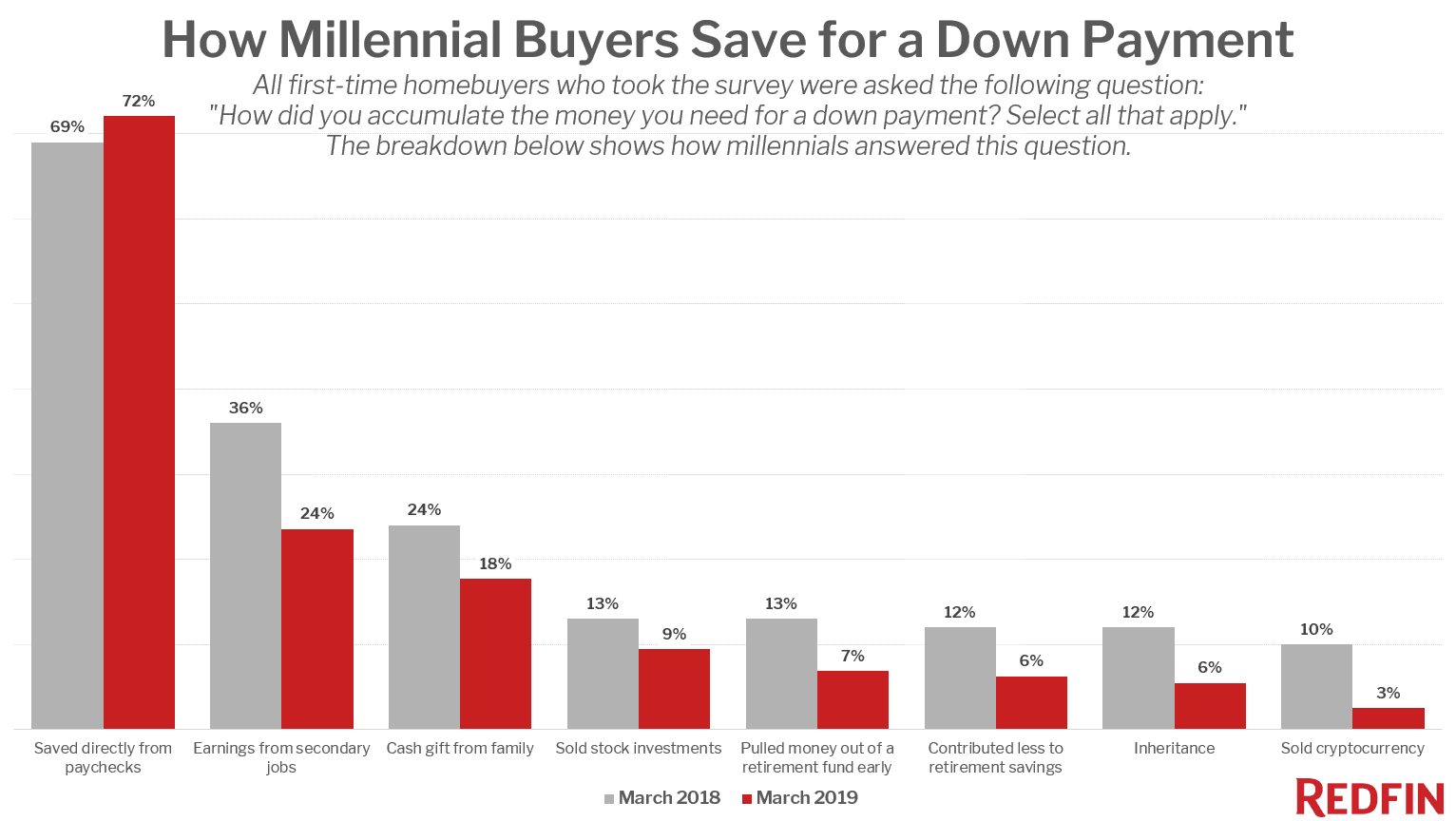

72% of millennial homebuyers are funding their down payment the old-fashioned way: saving from regular paychecks.

Twenty-four percent of millennial homebuyers took a second job to save for a down payment, down from 36 percent last year. This is according to a March survey commissioned by Redfin of over 2,000 U.S. residents who planned to buy or sell a primary residence in the next 12 months.

The findings in this report are based on the over 500 respondents to the survey who were born between 1981 and 1996, the generation commonly known as “millennials.” We compare the results with those from a similar survey we commissioned in March 2018. Both surveys asked all first-time homebuyers the question “How did you accumulate the money you need for a down payment? Select all that apply.” The results presented here are based on the answers that survey respondents selected to that question.

The fact that millennial homebuyers are increasingly able to save money for a down payment and becoming less reliant on non-traditional funding methods likely has to do with the fact that wage growth for American workers hit a 10-year high in February after several years when wage growth fell far short of home price growth.

The combination of strong wages and the housing market stalling late last year means that more buyers are able to save for their down payment using their primary income alone. Seventy-two percent of millennial homebuyers this year indicated they had saved for a down payment directly from their paychecks, up from 69 percent last year.

“Unemployment is at its lowest point since 2000,” said Redfin chief economist Daryl Fairweather. “Millennials have never worked in an economy this strong before, and are now finally making enough from their paychecks to save for a home. The fact that they are less often needing to rely on family members or sacrificing retirement savings to fund a home purchase is another sign that millennials are finally gaining their financial footing.”

It’s also notable that compared to a year ago, the share of millennial respondents who sold cryptocurrency to fund a down payment fell dramatically, from 10 percent last year to just 3 percent in 2019. This is likely due to a similarly dramatic decline in the price of the digital asset. In early 2018, Bitcoin, the most popular cryptocurrency, was trading at around $10,000 for one bitcoin. As of this past March, that had fallen to under $4,000.

In fact, compared to a year earlier, every category but saving from primary earnings declined:

- Received cash gifts from family: 18%, down from 24%

- Sold stock investments: 9%, down from 13%

- Pulled money from a retirement fund early: 7%, down from 13%

- Contributed less to retirement savings: 6%, down from 12%

- Received an inheritance: 6%, down from 12%

Source: redfin.com ~ By: Tim Ellis ~ Chart by redfin.com